- Impact Growth Capital Newsletter

- Posts

- Impact Growth Capital Newsletter

For Accredited Investors & Family Offices:

We do not market deals to the public.

We Grant Access to our specific investment thesis Barbell Strategy execution via Work Force Housing and Vertical SaaaS though our:

Investor Council

We are currently reviewing applications for new members. If you are focused on capital preservation and asymmetric growth, you may apply for access here.

This week at IGC:

This issue arrives at a moment of genuine market stress. A U.S.-Iran war has sent oil above $100 per barrel, effectively sidelined the Federal Reserve, and triggered a wave of redemption gates across private credit funds that now extends from BlackRock to Morgan Stanley.

These events are not isolated. They are interconnected, and the connections matter for how you think about portfolio positioning heading into Q2. Our goal with this publication is not to recap headlines you have already read. It is to connect the dots, identify what is mispriced, and give you a framework for acting with conviction when others are reacting.

Macro | Rates, Oil, and the Fed

The War Premium: Why Rate Cuts Are Off the Table

Markets have repriced from two Fed cuts to nearly zero in two weeks. The question is not whether inflation returns. It is whether growth survives it.

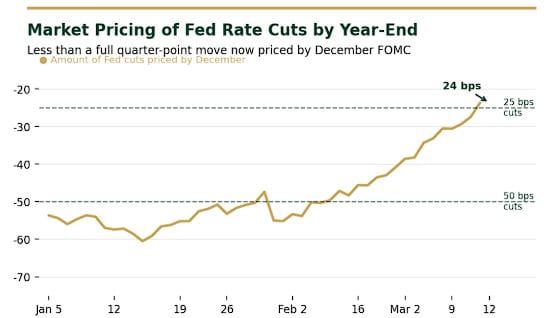

As recently as February 28, interest rate markets were pricing in 50 basis points of Federal Reserve easing by year end. Today that figure stands at 24 basis points — below the threshold of a single quarter-point cut. The repricing was triggered by the U.S. military campaign against Iran, which has closed the Strait of Hormuz and sent oil futures into territory not seen since August 2022.

WTI crude posted a 35% weekly gain, the largest in futures trading history dating to 1983. Brent crude crossed $100 per barrel after major Middle Eastern producers cut output in response to Hormuz disruptions. The two-year Treasury yield climbed to 3.71%, and 30-year paper is expected to clear near 4.88% at today's Treasury auction — the highest result since July.

The fiscal backdrop amplifies the problem. The Supreme Court struck down tariff collections on February 20, removing a revenue stream at precisely the moment a military campaign requires increased spending. More Treasury supply into an already soft market means upward pressure on long rates that mortgage markets, commercial real estate, and floating-rate borrowers will feel immediately.

Source: Bloomberg | IGC Intel Brief | March 12, 2026

Market pricing of Fed rate cuts by year-end. Source: Bloomberg

Portfolio Implication

Stress-Test Your Rate Assumptions Now

If you hold floating-rate exposure at the fund level or through direct lending positions, your cost of carry has just moved against you. Cap costs are rising, refinancing assumptions built on two Fed cuts this year should be stress-tested, and any asset dependent on a Q2 or Q3 rate relief rally needs a revised base case now.

Private Credit | Stress Is Structural, Not Temporary

Redemption Gates, Back Leverage, and the Valuation Gap

The private credit unwind has three distinct drivers operating simultaneously. Each one alone would be manageable. Together, they represent a feedback loop.

Driver 1: Investor Redemptions

Morgan Stanley and Cliffwater became the latest managers this week to cap investor withdrawals from private credit funds, following BlackRock's decision the prior week. The underlying cause is a wave of redemption requests from investors in semi-liquid vehicles — products marketed to high net worth individuals and family offices with the promise of private credit returns and more accessible liquidity than traditional drawdown structures. The liquidity profile of those products does not match the underlying loan portfolios, and funds are gating to protect remaining investors.

The Bank of France Governor identified this mismatch by name at Bloomberg's Future of Finance in Paris, pointing to recent defaults at First Brands Group, Tricolor Holdings, and Market Financial Solutions as evidence that credit quality deterioration is running ahead of fund-level marks.

Driver 2: Back Leverage Contraction

Back leverage is the mechanism by which private credit funds borrow against their loan portfolios to amplify returns. In normal conditions, back leverage can turn an 8 to 9 percent base return into double digits. It is the primary engine of the asset class's return profile and the main reason institutional capital flooded into the space over the past five years.

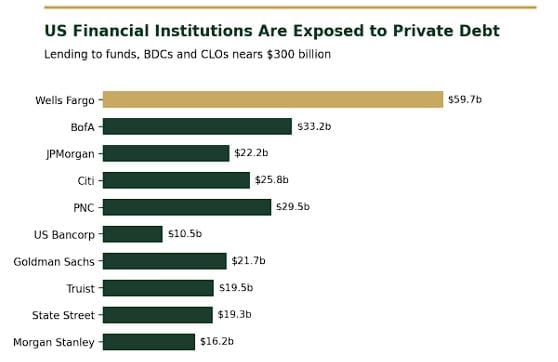

JPMorgan — which had uniquely negotiated the right to revalue private credit assets on its own timeline — has begun curbing lending against certain portfolios, particularly those with software company exposure under AI disruption pressure. Other major global banks are now in internal discussions about tightening their own facilities. Moody's estimates U.S. bank lending to private credit funds, BDCs, and CLOs stands near $300 billion. The Office of Financial Research puts the figure as high as $345 billion. Spreads currently sit around 150 basis points over SOFR, but refinancing discussions will likely push that figure toward the 275 basis point levels seen in 2024.

Source: Board of Governors of the Federal Reserve System and Moody’s Ratings, as of June 2025 IGC Intel Brief | March 12, 2026

U.S bank lending to private credit funds, BDCs, and CLOs. Source: Federal Reserve/ Moody’s

Driver 3: Valuation Opacity

Publicly traded BDCs are marking down loans, particularly in software and AI-adjacent credits. Private fund managers are holding stale valuations on economically similar positions. This gap is not sustainable. Banks, already under pressure from the Iran war macro environment, have little appetite to be the last sophisticated counterparty holding overmarked paper.

For Family Offices

Review Your Redemption Queue Position Now

If your allocation includes semi-liquid private credit vehicles from any of the major alternative asset managers, review your redemption queue position and the fund's gate provisions now — before the next quarterly window. Secondary market discounts on fund interests are widening and may represent an exit option at less cost than anticipated, or an entry for those with dry powder and patience.

Real Estate | The Affordability Window Closes

Mortgage Rates Reverse Course as Treasury Yields Jump

A brief moment of housing market optimism has given way to renewed rate pressure. Spring season projections require revision.

The 30-year fixed mortgage rate reached 6.11% this week, up from 6.00% last week — the largest single-week increase since April 2025. The reversal erases the sub-6% window that briefly opened in late February, which had raised hopes for a modestly improved spring selling season.

For residential operators and multifamily investors, the practical impact is two-dimensional. Buyer demand softens when rates move sharply higher, particularly when the move is abrupt rather than gradual. And on the debt side, agency and conduit pricing modeled on a two-cut Fed assumption needs to be reset.

The NAR's affordability index had reached its best reading since 2022 in February. That improvement is largely unwound. Bright MLS chief economist Lisa Sturtevant has publicly stated that spring market activity expectations are materially lower than a month ago. For operators planning disposition events in the next two quarters, extending hold assumptions and stress testing at 6.25 to 6.50 percent rates is prudent.

Acquisition Note

Motivated Sellers Are Coming

Distressed sellers who modeled exits at Q1 or Q2 rate assumptions may begin surfacing by late Q2 or early Q3. Investors with assumable debt at sub-5 percent rates on stabilized assets hold a meaningful structural advantage. The bid-ask spread is widening — which historically precedes motivated seller activity.

Global | European Banks Under Dual Pressure

Basel 3 Asymmetry and the Capital Flight Problem

European banking leadership is flagging not just the war, but a structural competitive disadvantage that predates it.

At Bloomberg's Future of Finance conference in Paris, Credit Mutuel Chairman Daniel Baal identified a potential inflationary shock from the Iran conflict as the primary near-term risk, noting that the ECB may be forced to raise rates rather than cut — which would compress lending margins across the continent.

Baal also flagged a structural concern: approximately 300 billion euros in European savings flow annually into U.S. markets due to the asymmetric application of Basel 3 capital requirements, which places European banks at a competitive disadvantage relative to their U.S. and U.K. counterparts.

Bank of France Governor Villeroy separately noted that some banks are marking down private credit holdings in software companies while fund managers maintain higher valuations on the same credits — a valuation gap that regulators are now monitoring with urgency alongside the semi-liquid retailization of private credit.

Strait of Hormuz Status

Every session of closure extends the oil shock and delays Fed rate cut expectations. Watch for credible ceasefire signals, G7 strategic petroleum reserve releases, or Trump's stated five-week timeline as the primary relief valve triggers.

Private Credit BDC Earnings

Marks are diverging between public BDCs and private fund vehicles. A second wave of redemption requests is likely if fund managers are forced to reconcile stale valuations under investor or lender pressure.

Today's 30-Year Treasury Auction

A clearing yield near 4.88% would be the highest since July and would set the tone for long-rate direction heading into Q2. Soft demand accelerates the fiscal premium embedded in mortgage rates and commercial real estate cap rate assumptions.

Morgan Stanley and BlackRock Gate Durations

How long the redemption caps remain in place is the clearest signal of whether this is a temporary liquidity squeeze or the beginning of a structural unwind in private credit.

ECB Guidance

If the ECB signals a pivot toward rate hikes driven by energy inflation, European credit and equity markets face another leg lower — with potential spillover into U.S. risk assets, particularly alternatives with European LP bases.

WHERE WE SEE OPPORTUNITY

The Barbell Holds

The macro environment described above is not uniformly negative. For investors positioned correctly before the dislocation, it is clarifying.

Workforce Housing

Private credit stress does not emerge in a vacuum. The capital that funded value-add multifamily acquisitions at compressed cap rates with floating-rate debt is now facing gate events, lender margin calls, and refinancing assumptions that no longer hold. Distressed sellers who modeled Q1 or Q2 exits are approaching capitulation. That creates an acquisition environment for operators with equity flexibility and assumable or fixed-rate debt structures — assets that cannot be replicated at origination in a 6-plus percent rate world.

At the same time, the affordability reversal described above means more households stay renters longer. Demand for workforce housing — non-luxury, institutionally managed multifamily — is structurally supported by the same rate environment that is breaking leveraged buyers. The durable cash flow thesis does not require a rate cut to perform. It requires supply scarcity and wage-earning tenants. Both remain intact.

Data Center and AI Infrastructure

The private credit unwind is concentrated in software and AI-adjacent credits — companies whose valuations were built on growth assumptions now being stress-tested by tighter capital and rising rates. That is not the same as stress in the physical infrastructure those companies depend on. Compute demand does not slow because lending conditions tighten. If anything, the shakeout accelerates consolidation toward larger, better-capitalized operators and the facilities they require.

Power-constrained, purpose-built data center assets with contracted tenants represent the asymmetric component of a barbell designed for exactly this environment — downside insulated by hard asset collateral, upside driven by a structural demand curve that a geopolitical shock does not reverse.

When private credit gates, long-duration Treasuries soften, and rate relief gets pushed out, investors look for yield that doesn't depend on a macro catalyst to materialize. Stabilized workforce housing cash flows and contracted infrastructure assets are two places that yield exists. That is the barbell. And right now, the barbell holds.

Jesse Sells

Founder | Impact Growth Capital